Retirement Frequently Asked Questions

Howard University Employees’ Retirement Plan (Defined Benefit Pension)

Do I qualify for a pension?

If you were hired prior to the close of the Howard University Employees’ Retirement Plan (the “Plan”) effective June 30, 2010, and meet eligibility and vesting requirements, you may qualify for a benefit.

What are the vesting and eligibility requirements of the pension plan?

Prior to the freeze date, eligible employees could participate in the Retirement Plan beginning on

January 1 or July 1 coinciding with or following the date he or she:

• reached age 25 effective July 1, 1976, amended to age 21 effective July 1,1985, service prior age is excluded and

• completed at least one year of service (a specified 12 consecutive month measurement period

in which the employee was credited with at least 1,000 hours of service).

• Vested with 10 years of service effective July 1,1976; amended to 5 years of service effective July 1, 1985

When can I commence my benefit?

Your normal retirement date is the June 30th coinciding with or following the later of the date you attain age 65 or have five years of Retirement Plan participation.

Your earliest commencement date is when the combination of your age and years of vesting service total to 70 or more.

What is early retirement?

You can apply to receive an early retirement benefit when the combination of your age and years

of vesting service total 70 or more. For example, you will qualify if you are age 55 and you have

15 years of vesting service (55 + 15 = 70).

Your early retirement benefit will be less than if you waited until your normal retirement date

because you will be receiving these payments over a longer period of time.

Your early retirement benefit is calculated by taking your normal retirement benefit and reducing

it by:

• Five-ninths of 1% for each of the first 60 months for which your benefit commencement

precedes your normal retirement date,

• Five-eighteenths of 1% for each of the next 60 months, and

• The Plan’s actuarial factors for each month before age 55.

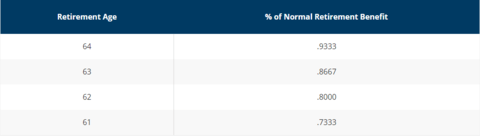

The following chart provides sample reduction amounts:

When was the cut off to receive pension?

The Retirement Plan was frozen effective as of June 30, 2010 (December 31, 2011 for certain participants represented by the AFSCME as described below)

• No new participants or rehired former participants can enter the Retirement Plan.

• You will not be credited with any additional credited service or receive additional benefit

accruals after that date. Compensation you earn after the freeze date is also not taken into

account under the Plan.

• If you were not vested as of the freeze date, you will continue to vest in your accrued benefit after the freeze date as long as you continue employment with the University or an affiliated employer.

Can I take a loan out of my pension?

No, loans are not permitted.

What is the procedure to retire?

Please contact the Human Resources Department at (202) 806-1280 to speak with a representative in the Retirement Department or email at RetirementHU@howard.edu , 90-days prior to your anticipated date to terminate employment or retire.

I am thinking about retirement, when and with whom should I speak with regarding retirement?

Please contact the Human Resources Department at (202) 806-1280 to speak with a representative in the Retirement Department or email at RetirementHU@howard.edu to discuss your retirement options:

- 5 years away from retiring

- 6 to 12 months away from retiring

Meet with a TIAA representative, at least annually, to discuss your current savings position and if there are any recommendations or adjustments to be made to prepare for your anticipated date of retirement. You may contact a TIAA representative at (800) 842-2252 or log in to your account at www.tiaa.org/Howard

How do I receive a letter for proof of pension?

Please contact the Human Resources Department at (202) 806-1280 to speak with a representative in the Retirement Department or email at RetirementHU@howard.edu to request a pension statement/verification.

When should I receive my pension payments?

Once all required documents have been submitted and your benefits are processed, the annuity payment is distributed the 15th of each month.

What benefits do I receive as a retiree?

- Eligible retirees receive the following benefits:

- tuition remission

- life insurance

- Age pre-65 only – medical/dental coverage

- participant qualified for normal/early/late retirement and commenced their annuity at separation of service.

Deferred Vested participants are not eligible for retiree benefits.

• Deferred Vested includes any participant that terminated employment and deferred the commencement of their annuity benefit for a later date.

Howard University Savings Plans (Defined Contribution)

What type of Savings Plans does Howard offer?

· 403(b) and 403(b) Roth Savings Plan

· 457(b) Deferred Compensation Plan

Does Howard University contribute to my savings plan?

Howard University contributes to your savings in two ways:

· The employer basic contribution in the sum equal to 6% of your eligible compensation from your date of hire.

· The employer match contribution equal to 50% of your employee elected deferral contribution, not to exceed 2% of your eligible compensation each pay period.

When am I vested in the Savings Plans?

You are immediately vested 100% at date of hire.

How do I enroll in the Savings Plans and set my employee deferral contributions?

If you are eligible, you are automatically enrolled into a TIAA 403(b) account to receive your 6% employer basic contributions effective the date of hire.

You may contact a TIAA representative at (800) 842-2252 or log in to your account at www.tiaa.org/Howard to set up your employee elected deferral contributions to receive the employer match and to adjust your asset allocations.

When can I take a cash distribution from my savings plan?

• Distributions can be made after you attain the age of 59 ½

• After separation from service

What is a Required Minimum Distribution (RMD)?

• The IRS requires that, after a certain point, you begin to withdraw from your 403(b)-retirement plan account.

• Money contributed and growing after 1986 has minimum distributions rules by April 1 of the year following the year in which you attain age 70 1/2, or following the year in which you retire, whichever is later.

• Money contributed and growing before 1986 has minimum distributions rules by April 1 of the year following the year in which you attain age 75, or following the year in which you retire, whichever is later.

• If you do not take the required minimum distribution, you may be subject to an excise tax as high as 50 percent on the amount you should have received in addition to our regular taxes.

• Contact your tax accountant and TIAA for more information.

Am I eligible to participate in the 457(b) Savings Plan?

You are eligible if you earn $150,000 or more annually and are scheduled to contribute the maximum annual tax deferred employee limit in your 403(b) savings plan.

If I left Howard University and I have a savings plan can I rollover my funds?

You may rollover the money in your TIAA savings plans to a qualified plan once you attain age 59 ½ or you terminate your employment.

Contact your Savings Plan vendor to discuss your options and tax implications.

How do I update my beneficiary for my savings plan?

You may update your beneficiary by accessing your account on www.tiaa.org/Howard.

What does “pre-tax” or “before-tax” mean?

The amount that you elect to have deducted for the 403(b) or 457 (b) is contributed to the plan before federal and state income tax, therefore reducing your taxable income, which may reduce the federal and state income taxes you pay each year.

The earnings on contributions grow tax deferred until you take a distribution. At that time both your contributions and earnings will be taxed as income.

What is a QDRO?

A QDRO, or a qualified domestic relations order, is a legal order which can follow a divorce or legal separation. This type of order splits ownership of a retirement account to give the alternate payee/ex-spouse a share of the assets.

You may access the forms on the website or by contacting the Human Resources Department at (202) 806-1280 to speak with a representative in the Retirement Department or email at RetirementHU@howard.edu to obtain model language or additional instructions pertaining to a QDRO.

Transfer to Single Record Keeper - TIAA

With the Transfer to TIAA, do I still need to utilize My Retirement Manager for a loan/hardship/distribution?

Effective November 4, 2019 all participants are to log in to www.tiaa.org/Howard to access their Savings Plan accounts to set up deferral contributions, asset allocations, request distributions, loans, hardships, and additional administrative and financial services (403(b), Roth, 457 (b)).

Will the Transfer to TIAA affect all active and retirees?

All participants with eligible funds invested in the Howard University Savings Plans will be mapped to the new TIAA platform. You may contact a TIAA representative at (800) 842-2252 to access personalized advice on the Plan’s investment options.

When will I be able to submit payroll deferral changes during the TIAA transition?

Effective November 4, 2019, salary deferral elections can be made online through TIAA.

Note: No salary deferral elections changes can be made from October 17, 2019 – November 3, 2019.

When can I access my new TIAA account and set up my beneficiaries?

You will have access to your account that you will automatically be enrolled in (the new Retirement Choice (RC) and/or Retirement Choice Plus (RCP) accounts) at TIAA on or around October 29, 2019.

IAA account Contribution source

1. Retirement Choice (RC) Basic employer contribution and employer match

2. Retirement Choice Plus (RCP) Basic and supplemental employee contributions

Note: Beneficiary designations will be set to “Estate,” so we encourage you to update your beneficiary information as soon as you are able.

Once the transfer to TIAA is complete, will I still have to use my retirement manager?

No, effective November 4, 2019, you may access and manage your account information on www.tiaa.org/Howard.

When is the Blackout Period?

The Blackout Period is expected to begin at both VALIC and Voya on or around November 5, 2019, at 4 p.m. (ET) and end on or before November 27, 2019.

What services are not available during the Blackout Period?

During this time, you will not be able to perform transactions (e.g., change investments, make withdrawals, take a loan, transfer funds).

Will my contributions continue during the Blackout Period?

Payroll contributions to the Plan will continue to be withheld during the Blackout Period.

When do my contribution start going to the new platform with TIAA?

Effective November 8, 2019 all contributions to the Plan will be directed to your new account with TIAA

If I am a Howard University retiree and I am receiving my funds from Valic/Voya, what happens to my funds when Howard University transfers over to TIAA?

• Account balances from VALIC/Voya will be applied to the new investment options on the TIAA platform.

• Upon the completion of the transfers, you will typically receive two confirmations: one from VALIC/Voya showing the transfer out of your account(s); and one from TIAA, showing the balance(s) applied to your new TIAA account(s).

• VALIC participants: On or around November 14, 2019, your account balance(s) will transfer to your new TIAA account. Fixed and variable annuities, including the Fixed Account Plus, will not transfer automatically and you will have to contact TIAA to request the transfer of these particular accounts.

• Voya participants: On or around November 13, 2019, your account balance(s) with Voya are scheduled to be transferred to your new TIAA account.

How do I make an appointment with a TIAA representative?

• Call TIAA at 800-842-2252, weekdays, 8 a.m. to 10 p.m., and Saturday, 9 a.m. to 6 p.m. (ET).

• Make an appointment with a TIAA financial consultant. Visit TIAA.org/schedulenow, or call 800-732-8353, weekdays, 8 a.m. to 8 p.m. (ET).

How do I compare my investment with the new investment platform with TIAA?

For details, see the account comparison chart at TIAA.org/comparison. If you have questions, call 800-842-2252.